Free CIMA CIMAPRO19-P01-1 Actual Exam Questions

Dumps Box (DumpsBox) offers up-to-date practice exam questions for CIMAPRO19-P01-1 certification exam which are developed and validated by CIMA subject domain experts certified in CIMA CIMAPRO19-P01-1 . These practice questions are update regularly as we keep an eye on any recent changes in CIMAPRO19-P01-1 syllabus, and when there is update our team quickly adjusts the questions. This commitment to providing the best quality exam prep material to certification aspirants is what makes DumpsBox.com the best certification exam prep website. On top of that, our strong, yet strictly moderated, community based feedback keeps the content clean and current. Each question has helpful community discussion that provides it extra perspective and introduces helpful resources for better exam preparation. This also saves students from other outdated practice questions or illicit exam dumps that can have adverse affects on career. Browse through our CIMA CIMAPRO19-P01-1 exam questions and pass your exam on first try.

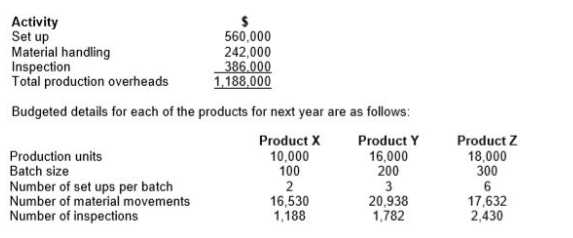

budgeted for next year:

Required:

Calculate the total budgeted production overhead cost for each product using activity based

budgeting.

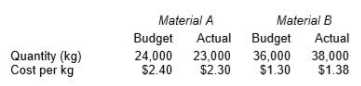

material quantities and costs for August are given in the table below.

Budgeted and actual output of the product for August was 12,000 units.

The material yield variance for August is:

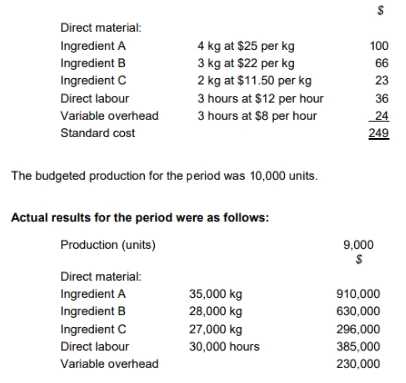

to the customers’ specific requirements. The standard cost per unit of its most popular cake is as

follows:

The general market prices at the time of purchase for Ingredient A and Ingredient B were $23 per kg

and $20 per kg respectively. TP operates a JIT purchasing system for ingredients and a JIT production

system; therefore, there was no inventory during the period.

Discuss the usefulness of the planning and operational variances calculated for TP’s management.

Select ALL the TRUE statements.

if he is not seen to have needed all the funds. He decides to spend the remaining £1,580 on another

team building exercise as well as a catered lunch for his department.

This example falls under which behavioural aspect of budgetary control?

management accountant is considering introducing a standard costing system.

Which THREE of the following are reasons that support the case for the company's introduction of a

standard costing system?

‘A zero-based budgeting system involves establishing decision packages that are then ranked in order of their relative importance in meeting the organization’s objectives’. Which of the following is true regarding he difficulties that a not-for-profit organization may experience when trying to rank decision packages. Select ALL true statements.

Consequently, they should use an approach to budgeting other than incremental budgeting.’

Required:

Explain ONE advantage and TWO disadvantages of public sector organizations using incremental

budgeting.

Select all true statements.

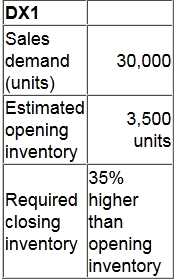

The following information is available:

How many units of the DX1 will need to be produced in the forthcoming year?

According to a decision tree forecasting, there are three possible outcomes of a project requiring £10,000 capital investment. They are (along with probability of occurring): £20,000 in revenue (45%), £35,000 (15%), £10,000 (30%) and -£6,000 (10%). However, choosing another project (2) requiring the same investment would give us £12,000 and choosing project 3 would give us a 90% chance of generating revenues of £15,000 but a 5% chance of revenues of £0. Project 4 is wildly ambitious and boasts an unlikely (5% chance) of generating revenues of £100,000. There is a 10% probability of negative revenues. Which is the risk averse investor more likely to take?

marginal costing because ABC:

RFT, an engineering company, has been asked to provide a quotation for a contract to build a new engine. The potential customer is not a current customer of RFT, but the directors of RFT are keen to try and win the contract as they believe that this may lead to more contracts in the future. As a result, they intend pricing the contract using relevant costs. The following information has been obtained from a two-hour meeting that the Production Director of RFT had with the potential customer. The Production Director is paid an annual salary equivalent to $1,200 per 8-hour day. 110 square meters of material A will be required. This is a material that is regularly used by RFT and there are 200 square meters currently in inventory. These were bought at a cost of $12 per square meter. They have a resale value of $10.50 per square meter and their current replacement cost is $12.50 per square meter. 30 liters of material B will be required. This material will have to be purchased for the contract because it is not otherwise used by RFT. The minimum order quantity from the supplier is 40 liters at a cost of $9 per liter. RFT does not expect to have any use for any of this material that remains after this contract is completed. 60 components will be required. These will be purchased from HY. The purchase price is $50 per component. A total of 235 direct labour hours will be required. The current wage rate for the appropriate grade of direct labour is $11 per hour. Currently RFT has 75 direct labour hours of spare capacity at this grade that is being paid under a guaranteed wage agreement. The additional hours would need to be obtained by either (i) overtime at a total cost of $14 per hour; or (ii) recruiting temporary staff at a cost of $12 per hour. However, if temporary staff are used they will not be as experienced as RFT’s existing workers and will require 10 hours supervision by an existing supervisor who would be paid overtime at a cost of $18 per hour for this work. 25 machine hours will be required. The machine to be used is already leased for a weekly leasing cost of $600. It has a capacity of 40 hours per week. The machine has sufficient available capacity for the contract to be completed. The variable running cost of the machine is $7 per hour. The company absorbs its fixed overhead costs using an absorption rate of $20 per direct labour hour. Select ALL the true statements.

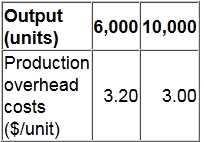

The following details are available for a company's production overhead costs at different levels of activity:  The company uses the high-low method to calculate its budgeted production overhead costs. What is the budget for production overhead costs at an activity level of 8,500 units? Give your answer as a whole number.

The company uses the high-low method to calculate its budgeted production overhead costs. What is the budget for production overhead costs at an activity level of 8,500 units? Give your answer as a whole number.

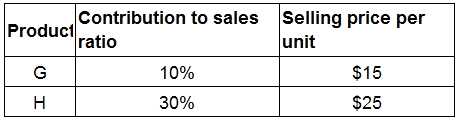

Information about a company's two products is as follows:  The products are currently sold in equal quantities. Monthly fixed costs are $360,000. What is the monthly breakeven sales revenue assuming a sales quantity mix of 50/50? Give your answer to the nearest $.

The products are currently sold in equal quantities. Monthly fixed costs are $360,000. What is the monthly breakeven sales revenue assuming a sales quantity mix of 50/50? Give your answer to the nearest $.

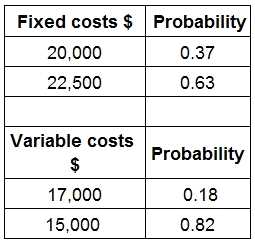

GP is launching a new product. The annual forecast costs are as follows:  What is the expected value of the total costs? Give your answer to the nearest whole $.

What is the expected value of the total costs? Give your answer to the nearest whole $.