Free CFA-Institute CFA Level II Actual Exam Questions

Dumps Box (DumpsBox) offers up-to-date practice exam questions for CFA Level II certification exam which are developed and validated by CFA Institute subject domain experts certified in CFA-Institute CFA Level II . These practice questions are update regularly as we keep an eye on any recent changes in CFA Level II syllabus, and when there is update our team quickly adjusts the questions. This commitment to providing the best quality exam prep material to certification aspirants is what makes DumpsBox.com the best certification exam prep website. On top of that, our strong, yet strictly moderated, community based feedback keeps the content clean and current. Each question has helpful community discussion that provides it extra perspective and introduces helpful resources for better exam preparation. This also saves students from other outdated practice questions or illicit exam dumps that can have adverse affects on career. Browse through our CFA-Institute CFA Level II exam questions and pass your exam on first try.

world, and its foreign currency department trades more currency on a daily basis than any other

firm. Gillis specializes in currencies of emerging nations.

Gillis received an invitation from the new Finance Minister of Binaria, one of the emerging nations

included in Gillis's portfolio. The minister has proposed a number of fiscal reforms that he hopes will

help support Binaria's weakening currency. He is asking currency specialists from several of the

largest foreign exchange banks to visit Binaria for a conference on the planned reforms. Because of

its remote location, Binaria will pay all travel expenses of the attendees, as well as lodging in

government-owned facilities in the capital city. As a further inducement, attendees will also receive

small bags of uncut emeralds (as emeralds are a principal export of Binaria), with an estimated

market value of $500.

Gillis has approximately 25 clients that she deals with regularly, most of whom are large financial

institutions interested in trading currencies. One of the services Gillis provides to these clients is a

weekly summary of important trends in the emerging market currencies she follows. Gillis talks to

local government officials and reads research reports prepared by local analysts, which are paid for

by Trent. These inputs, along with Gillis's interpretation, form the basis of most of Gillis's weekly

reports.

Gillis decided to attend the conference in Binaria. In anticipation of a favorable reception for the

proposed reforms, Gillis purchased a long Binaria currency position in her personal account before

leaving on the trip. After hearing the finance minister's proposals in person, however, she decides

that the reforms are poorly timed and likely to cause the currency to depreciate. She issues a

negative recommendation upon her return. Before issuing the recommendation, she liquidates the

long position in her personal account but does not take a short position.

Gillis's supervisor, Steve Howlett, CFA, has been reviewing Gillis's personal trading. Howlett has not

seen any details of the Binaria currency trade but has found two other instances in the past year

where he believes Gillis has violated Trent's written policies regarding trading in personal accounts.

One of the currency trading strategies employed by Trent is based on interest rate parity. Trent

monitors spot exchange rates, forward rates, and short-term government interest rates. On the rare

occasions when the forward rates do not accurately reflect the interest differential between two

countries, Trent places trades to take advantage of the riskless arbitrage opportunity. Because Trent

is such a large player in the exchange markets, its transactions costs are very low, and Trent is often

able to take advantage of mispricings that are too small for others to capitalize on. In describing

these trading opportunities to clients, Trent suggests that "clients willing to participate in this type of

arbitrage strategy are guaranteed riskless profits until the market pricing returns to equilibrium."

Trent's arbitrage trading based on interest rate parity is successful mostly due to Trent's large size,

which provides it with an advantage relative to smaller, competing currency trading firms. Has Trent

violated CFA Institute Standards of Professional Conduct with respect to its trading strategy or its

guarantee of results?

the United States and Canada. The firm's software provides an integrated solution to monitoring,

analyzing, and managing output from a variety of diagnostic medical equipment including MRls, CT

scans, and EKG machines. MediSoft has grown rapidly since its inception ten years ago, averaging

25% growth in sales over the last decade. The company went public three years ago. Twelve months

after their IPO, MediSoft made two semiannual coupon bond offerings, the first of which was a

convertible bond. At the time of issuance, the convertible bond had a coupon rate of 7.25%, par

value of $1,000, a conversion price of $55.56, and ten years until maturity. Two years after issuance,

the bond became callable at 102% of par value. Soon after the issuance of the convertible bond, the

company issued another series of bonds which were putable, but contained no conversion or call

features. The putable bonds were issued with a coupon of 8.0%, par value of $1,000, and 15 years

until maturity. One year after their issuance, the put feature of the putable bonds became active,

allowing the bonds to be put at a price of 95% of par value, and increasing linearly over five years to

100% of par value. MediSoft's convertible bonds are now trading in the market for a price of $947

with an estimated straight value of $917. The company's putable bonds are trading at a price of

$1,052. Volatility in the price of MediSoft's common stock has been relatively high over the last few

months. Currently the stock is priced at $50 on the New York Stock Exchange and is expected to

continue its annual dividend in the amount of $1.80 per share.

High-tech industry analysts for Brown & Associates, a money management firm specializing in fixed-

income investments, have been closely following MediSoft ever since it went public three years ago.

In general, portfolio managers at Brown & Associates do not participate in initial offerings of debt

investments, preferring instead to see how the issue trades before considering taking a position in

the issue. Since MediSoft's bonds have had ample time to trade in the marketplace, analysts and

portfolio managers have taken an interest in the company's bonds. At a meeting to discuss the merits

of MediSofVs bonds, the following comments were made by various portfolio managers and analysts

at Brown & Associates:

"Choosing to invest in MediSoft's convertible bond would benefit our portfolios in many ways, but

the primary benefit is the limited downside risk associated with the bond. Since the straight value

will provide a floor for the value of the convertible bond, downside risk is limited to the difference

between the market price of the bond and the straight value."

"Decreasing volatility in the price of MediSoft's common stock as well as increasing volatility in the

level of interest rates are expected in the near future. The combined effects of these changes in

volatility will be a decrease in the price of MediSoft's putable bonds and an increase in the price of

the convertible bonds. Therefore, only the convertible bonds would be a suitable purchase."

Assuming that portfolio managers at Brown & Associates purchased the convertible bonds, how

many years would it take to recover the premium per share?

Juanita Chevas, CFA, in the currency trading department. Together, Wilson and Chevas are working

on the development of new trading software designed to detect profitable opportunities in the

foreign exchange market. Obviously, they are interested in risk-free arbitrage opportunities.

However, they have also been instructed to investigate the possibility of longer-term currency

exposures that are not necessarily risk-free. To test the logic of their new software, Wilson gathers

the following market data:

• Spot JPY/USD exchange rate = 120.

• Spot EUR/USD exchange rate = 0.7224.

• U.S. risk-free interest rate = 7%.

• Eurozone risk-free rate = 9.08%.

• Japanese risk-free rate = 3.88%.

• Yield curves in all three currencies are flat.

In addition to in-house currency transactions, the new software program is also intended to provide

insight into currency exposure and hedging needs for the bank's major customers. These customers

typically include large multinational firms. Essentially, the bank wants to provide consulting services

to its clients concerning which currency exposures offer the greatest possibility of appreciation. In

this process, the bank will rely on deviations from international parity conditions as an indicator of

long-term currency movements.

Wilson obtains the following data from the econometrics department:

• JPY/USD spot rate one year ago =116.

• EUR/USD spot rate one year ago = 0.7200.

• Anticipated and historical U.S. annual inflation = 3%.

• Anticipated and historical Japanese annual inflation = 0%.

• Anticipated and historical Eurozone annual inflation = 5%.

One of the bank's major customers has significant portions of its business in Japan, and the Eurozone

and has long exposure to both currencies. The customer has traditionally hedged all currency risk.

However, the customer's new risk manager has decided to leave some currency exposure unhedged

in an attempt to profit from long-term currency exposure.

Wilson wants to approximate the forward discount/premium for the JPY against the USD 12 months

from now. According to the approximate version of interest rate parity, the JPY would most likely

trade at a:

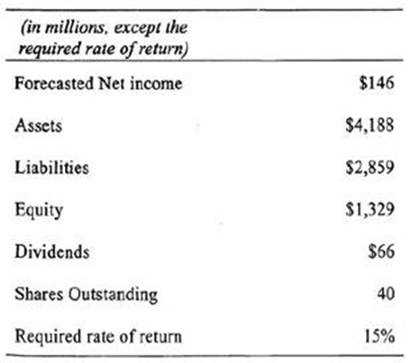

managers at her firm. If economic conditions warrant, she will update the parameters even more

frequently. As a result of an economic slowdown, she is going through this process now.

The firm has been using an equity risk premium of 5.6%, found with historical estimates. Tang is

going to use an estimate of the equity risk premium found with a macroeconomic model. By

comparing the yields on nominal bonds and real bonds, she estimates the inflation rate to be 2.6%.

She expects real domestic growth to be 3.0%. Tang does not expect a change in price/earnings ratios.

The yield on the market index is 1.7% and the expected risk-free rate of return is 2.7%.

Elizabeth Trotter, one of the firm's portfolio Managers, asks Tang about the effects of survivorship

bias on estimates of the equity risk premium. Trotter asks, "Which method is most susceptible to this

bias, historical estimates, Gordon growth model estimates, or survey estimates?"

Tang wishes to estimate the required rate of return for Northeast Electric (NE) using the Capital Asset

Pricing Model (CAPM) and the Fama-French three factor model. She is using the following

information to accomplish this:

· The risk-free rate of return is 2.7%.

· The expected risk premiums arc:

· The beta coefficient in the CAPM is estimated to be 0.63.

· The betas (factor sensitivities) for the three Fama-French factors are 1.00 for the market factor, -

0.76 for the size factor, and -0.04 for the book-to-markct factor.

Trotter also asks Tang about adjusted betas. She says, "We use a formula for the adjusted beta where

the adjusted beta = (2/3) (regression beta) + (1/3) (1.0). How do the adjusted betas compare to the

original regression betas?"

Trotter has one final question for Tang. Trotter says, "We need to estimate the equity beta for VixPRO,

which is a private company that is not publicly traded. We have identified a publicly traded company

that has similar operating characteristics to VixPRO and we have estimated the beta for that

company using regression analysis. We used the return on the public company as the dependent

variable and the return on the market index as the independent variable. What steps do I need to

take to find the beta for VixPRO equity? The companies have different debt/equity ratios. The debt of

both companies is very low risk, and I believe I can ignore taxes."

The estimate of the equity risk premium found with a macroeconomic model and the estimates

determined by Tang is closest to:

of studies for her MBA, She took the Level 3 CFA® exam in June but has not yet received her score.

Garvey's work involves preparing research reports on small companies.

Garvey is at lunch with a group of co-workers. She listens to their conversation about various stocks

and takes note of a comment from Tony Topel, a veteran analyst. Topel is talking about Vallo

Engineering, a small stock he has tried repeatedly to convince the investment director to add to the

monitored list. While the investment director does not like Vallo, Topel has faith in the company and

has gradually accumulated 5,000 shares for his own account. Another analyst, Mary Kennedy, tells

the group about Koral Koatings, a paint and sealant manufacturer. Kennedy has spent most of the last

week at the office doing research on Koral. She has concluded that the stock is undervalued and

consensus earnings estimates are conservative. However, she has not filed a report for Samson, nor

does she intend to. She said she has purchased the stock for herself and advises her colleagues to do

the same. After she gets back to the office, Garvey purchases 25 shares of Vallo and 50 shares of

Koral for herself.

Samson pays its interns very little, and Garvey works as a waitress at a diner in the financial district

to supplement her income. The dinner crowd includes many analysts and brokers who work at

nearby businesses. While waiting tables that night, Garvey hears two employees of a major

brokerage house discussing Metrona, a nanotechnology company. The restaurant patrons say that

the broker's star analyst has issued a report with a buy rating on Metrona that morning. The diners

plans to buy the stock the next morning. After Garvey finishes her shift, restaurant manager Mandy

Jones, a longtime Samson client, asks to speak with her. Jones commends Garvey for her hard work

at the restaurant, praising her punctuality and positive attitude, and offers her two tickets to a

Yankees game as a bonus.

The next morning, Garvey buys 40 shares of Metrona for her own account at the market open. Soon

afterward, she receives a call from Harold Koons, one of Samson's largest money-management

clients. Koons says he got Garvey's name from Bertha Witt, who manages the Koons' account. Koons

wanted to reward the analyst who discovered Anvil Hammers, a machine-tool company whose stock

soared soon after it was added to his portfolio. Garvey prepared the original report on Anvil

Hammers. Koons offers Garvey two free round-trip tickets to the city of her choice. Garvey thanks

Koons, then asks her immediate supervisor, Karl May, about the gift from Koons but does not

mention the gift from Jones. May approves the Koons' gift.

After talking with May, Garvey starts a research project on Zenith Enterprises, a frozen-juice maker.

Garvey's gathers quarterly data on the company's sales and profits over the past two years. Garvey

uses a simple linear regression to estimate the relationship between GDP growth and Zenith's sales

growth. Next she uses a consensus GDP estimate from a well-known economic data reporting service

and her regression model to extrapolate growth rates for the next three years.

Later that afternoon, Garvey attends a company meeting on the ethics of money management. She

listens to a lecture in which John Bloomquist, a veteran portfolio manager, talks about his job

responsibilities. Garvey takes notes that include the following three statements made by Bloomquist:

Statement 1: I'm not a bond expert, and I've turned to a colleague for advice on how to manage the

fixed-income portion of client portfolios.

Statement 2: I strive not to favor either the remaindermen or the current-income beneficiaries,

instead I work to serve both of their interests.

Statement 3: All of my portfolios have target growth rates sufficient to keep ahead of inflation.

Garvey is not working at the diner that night, so she goes home to work on her biography for an

online placement service. In it she makes the following two statements:

Statement 1: I'm a CFA Level 3 candidate, and I expect to receive my charter this fall. The CFA

program is a grueling, 3-part, graduate-level course, and passage requires an expertise in a variety of

financial instruments as well as knowledge of the forces that drive our economy and financial

markets.

Statement 1: I expect to graduate with my MBA from Braxton College at the end of the fall semester.

As both an MBA and a CFA, I'll be in high demand. Hire me now while you still have the chance.

During the lunch conversation, which CFA Institute Standard of Professional Conduct was most likely

violated?

merits of the developing hospice industry. The hospice industry has a short history in the public

market, as several companies have recently completed their initial public offering. Hospice services

are provided to patients diagnosed with terminal illness as an alternative to aggressive medical

management. The use of hospice services at skilled nursing facilities and assisted-living facilities is

forecasted to continue its recent growth. Medicare is the primary payer for hospice services,

accounting for 85% of the approximately $7 billion in industry's revenues. Hospice providers offer

symptom and pain management to patients diagnosed with a terminal illness by their physician. The

program was added to the Medicare benefit package in the early 1980s. Growth in the sector has

only recently. accelerated due to the emergence of a number of for-profit companies. The caregiver

provides a plan for each admitted patient and care is given in any number of healthcare

environments, including the patient's home.

Grass's analysis of the hospice industry has uncovered several facts that are outlined below:

• The industry's revenue annual growth rate has increased from 14% in the late 1990s to 25% in

2008.

• The average length of stay at facilities for hospice patients is increasing.

• Labor costs account for 75% of total expenses, drugs 15% of total expenses, and medical supplies

10%.

• More than 80% of hospice patients are above 65 years old and 30% are above 85 years old.

• Based on the U.S. Census Bureau's statistics, over the next six years (2009-2015), the number of

people in the 65 and older age group will increase annually by 1.4%.

• The Medicare hospice benefit is still underutilized by the terminally ill population, according to

MedPac (an independent advisory committee for the U.S. Congress on healthcare issues).

• Only 30% of Medicare beneficiaries enroll in the hospice benefit before they die.

• In recent years, the U.S. government has approved rate increases for the sector compared to flat or

declining rate trends for other healthcare services.

• The Medicare hospice program has a beneficiary cap which cannot exceed approximately $18,000

annually per person.

• The top six for-profit providers account for about half of the segment's sales.

• The overall hospice provider market is roughly divided into 55% non-profit, 10% U.S. government,

and 35% for-profit.

Grass's analysis has narrowed his search to Hope Company. Hope controls about 7% of the total

hospice service market or 20% of the for-profit market. The company has the only regulator

approved for-profit certificate for the state of Florida, one of the most attractive markets in the

United States. In addition to a strong market share in Florida, Hope has a strong presence in urban

markets like Dallas and San Francisco. Hope has a more diversified revenue base than other publicly

traded for-profit providers.

Grass's research report on Hope Company is positive on its investment merits. Grass's report states,

"Hope is uniquely positioned in the hospice industry" Which of the following best supports his

comment?

managers at her firm. If economic conditions warrant, she will update the parameters even more

frequently. As a result of an economic slowdown, she is going through this process now.

The firm has been using an equity risk premium of 5.6%, found with historical estimates. Tang is

going to use an estimate of the equity risk premium found with a macroeconomic model. By

comparing the yields on nominal bonds and real bonds, she estimates the inflation rate to be 2.6%.

She expects real domestic growth to be 3.0%. Tang does not expect a change in price/earnings ratios.

The yield on the market index is 1.7% and the expected risk-free rate of return is 2.7%.

Elizabeth Trotter, one of the firm's portfolio Managers, asks Tang about the effects of survivorship

bias on estimates of the equity risk premium. Trotter asks, "Which method is most susceptible to this

bias, historical estimates, Gordon growth model estimates, or survey estimates?"

Tang wishes to estimate the required rate of return for Northeast Electric (NE) using the Capital Asset

Pricing Model (CAPM) and the Fama-French three factor model. She is using the following

information to accomplish this:

· The risk-free rate of return is 2.7%.

· The expected risk premiums arc:

· The beta coefficient in the CAPM is estimated to be 0.63.

· The betas (factor sensitivities) for the three Fama-French factors are 1.00 for the market factor, -

0.76 for the size factor, and -0.04 for the book-to-markct factor.

Trotter also asks Tang about adjusted betas. She says, "We use a formula for the adjusted beta where

the adjusted beta = (2/3) (regression beta) + (1/3) (1.0). How do the adjusted betas compare to the

original regression betas?"

Trotter has one final question for Tang. Trotter says, "We need to estimate the equity beta for VixPRO,

which is a private company that is not publicly traded. We have identified a publicly traded company

that has similar operating characteristics to VixPRO and we have estimated the beta for that

company using regression analysis. We used the return on the public company as the dependent

variable and the return on the market index as the independent variable. What steps do I need to

take to find the beta for VixPRO equity? The companies have different debt/equity ratios. The debt of

both companies is very low risk, and I believe I can ignore taxes."

The required rate of return for NE estimated with the Fama-French three factor model is closest to:

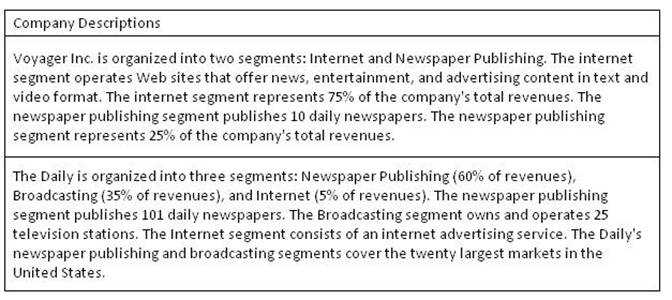

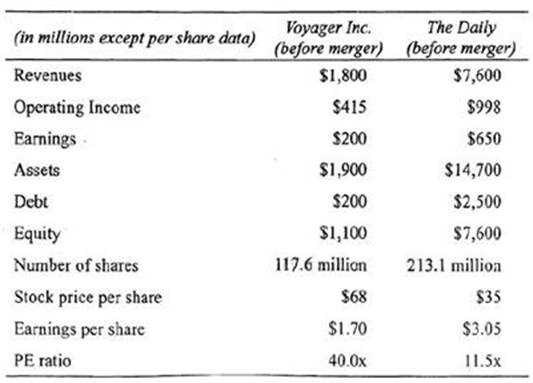

exposure to newspapers, television, and the internet.

Voyager's acquisition of The Daily is The company's second major acquisition in its history. The

previous acquisition was at the height of the merger boom in the year 2000. Voyager purchased the

Dragon Company at a premium to net asset value, thereby doubling the company's size. Voyager

used the pooling method to account for the acquisition of Dragon; however, because of FASB

changes to the Business Combination Standard, Voyager will use the acquisition method to account

for the Daily acquisition.

Voyager has made an all-cash offer of $45 per share to acquire The Daily. Wall Street is skeptical

about the merger. While Voyager has been growing its revenues by 40% per year, The Daily's revenue

growth has been less than 2% per year. Michael Renner. the CFO of Voyager, defends the acquisition

by stating that The Daily has accumulated a large amount of tax losses and that the combined

company can benefit by immediately increasing net income after the merger. In addition, Renner

states that the New Voyager will eliminate the inefficiencies of the internet operations and thereby

boost future earnings. Renner believes that the merged companies will have a value of $17.5 billion.

In the past, The Daily's management has publicly stated its opposition to merging with any company,

a position management still maintains. As a result of this situation, Voyager submitted their merger

proposal directly to The Daily's board of directors, while the firm's CEO was on vacation. Upon

returning from vacation, The Daily's CEO issued a public statement claiming that the proposed

merger was unacceptable under any circumstances.

Which of the following best characterizes Voyager's proposal to merge with The Daily?

catering to high net worth U.S. investors. She is assisted by Morgan Greene and Cathy Wong. Both

Greene and Wong have prepared their preliminary security selections and are meeting along with

Palmer today for detailed security analysis and valuation. They have narrowed their focus to a few

closed-end country funds and some firms from Switzerland, Germany, the U.K. and the emerging

markets.

The initial decision is to choose between closed-end country funds and direct investment in foreign

stock markets. Wong is in favor of country funds because:

1. Country funds provide immediate diversification.

2. Buying country funds is a better choice than direct investment for most emerging markets.

However, Wong has observed a premium to NAV that is prevalent in closed-end country funds. Wong

is curious as to how the observed premiums would affect investments in such instruments.

In contrast to Wong, Greene is more inclined towards individual stocks and has started looking into

their financial statements. One firm Greene is analyzing is a German conglomerate. Kaiser Corp.

Kaiser has a history of growing by acquiring high-growth firms in niche markets. Exhibit 1 provides

key financial information from Greene's analysis of Kaiser Corp.

Exhibit 1: Financial information—Kaiser Corp.

While going through their sample of emerging market stocks, Wong observed that these markets in

general have high inflation and that sales for the stocks were extremely seasonal. Wong

compensated by adjusting reported sales growth in the emerging market firms by deflating the sales

using annual inflation adjustments. Wong also made upward adjustments to reported depreciation

figures.

Wong suggested to her colleagues that they add a country risk premium to the discount rate they

were using to evaluate emerging market stocks. She further suggested that they estimate country

risk premiums by calculating the spread between the yield of U.S. government bonds and that of

similar maturity local bonds.

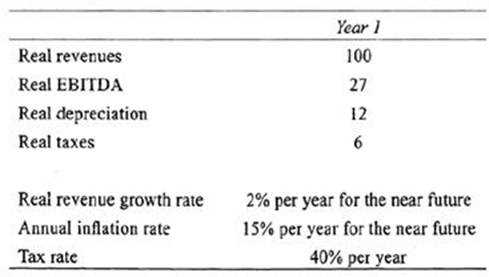

Subsequently they started working on the financial projections for Emerjico, Inc., an emerging

market stock. Their assumptions are given in Exhibit 2.

Exhibit 2: Key Assumptions—Emerjico

Based on Exhibit 1 and using the dividend discount model (DDM), the intrinsic value of Kaiser Corp is

closest to:

a potential investment recommendation of their common stocks. He is particularly concerned about

the quality of each company's financial results in 2007-2008 and in developing projections for 2009

and 2010 fiscal years.

Adams Company has been the largest company in the industry but Jefferson Inc. has grown more

rapidly in recent years. Adams's net sales in 2004 were 33-1/3% higher than Jefferson but were only

18% above Jefferson in 2008. During 2008, a slowing U.S. economy led to lower domestic revenue

growth for both companies. The 10-k reports showed overall sales growth of 6% for Adams in 2008

compared to 7% for 2007 and 9% in 2006. Jefferson's gross sales rose almost 12% in 2008 versus 8%

in 2007 and 10% in 2006. In the past three years, Jefferson has expanded its foreign business at a

faster pace than Adams. In 2008, Jefferson's growth in overseas business was particularly impressive.

According to the company's 10-k report, Jefferson offered a sales incentive to overseas customers.

For those customers accepting the special sales discount, Jefferson shipped products to specific

warehouses in foreign ports rather than directly to those customers' facilities.

In his initial review of Adams's and Jefferson's financial statements, Jones was concerned about the

quality of the growth in Jefferson's sales, considerably higher accounts receivables, and the impact of

overall accruals on earnings quality. He noted that Jefferson had instituted an accounting change in

2008. The economic life for new plant and equipment investments was determined to be five years

longer than for previous investments. For Adams, he noted that the higher level of inventories at the

end of 2008 might be cause for concern in light of a further slowdown expected in the U.S. economy

in 2009.

The accompanying table shows financial data for both companies' Form 10-k reports for 2006-2008

used by Jones for his analysis. To evaluate sales quality, he focused on trends in sales and related

expenses for both companies as well as cash collections and receivables comparisons. Inventory

trends relative to sales and the number of days' sales outstanding in inventory were determined for

both companies. Expense trends were examined for Adams and Jefferson relative to sales growth

and accrual ratios on a balance sheet and cash flow basis were developed as overall measures of

earnings quality.

The quality of earnings as measured by balance sheet based accruals ratios showed:

and investment banking services company. Wilson is reviewing two investment reports written by

Peter Holly, CFA, an analyst and portfolio manager who has worked for Excess for four years. Holly's

first report under compliance review is a strong buy recommendation for BlueNote Inc., a musical

instrument manufacturer. The report states that the buy recommendation is applicable for the next 6

to 12 months with an average level of risk and a sustainable price target of $24 for the entire time

period. At the bottom of the report, an e-mail address is given for investors who wish to obtain a

complete description of the firm's rating system. Among other reasons supporting the

recommendation, Holly's report states that expected increases in profitability as well as increased

supply chain efficiency provide compelling support for purchasing BlueNote.

Holly informs Wilson that he determined his conclusions primarily from an intensive review of

BlueNote's filings with the SEC but also from a call to one of BlueNote's suppliers who informed Holly

that their new inventory processing system would allow for more efficiency in supplying BlueNote

with raw materials. Holly explains to Wilson that he is the only analyst covering BlueNote who is

aware of this information and that he believes the new inventory processing system will allow

BlueNote to reduce costs and increase overall profitability for several years to come.

Wilson must also review Holly's report on BigTirae Inc., a musical promotions and distribution

company. In the report, Holly provides a very optimistic analysis of BigTime's fundamentals. The

analysis supports a buy recommendation for the company. Wilson finds one problem with Holly's

report on BigTime related to Holly's former business relationship with BigTime Inc. Two years before

joining Excess, Holly worked as an investment banker and received 1,000 restricted shares of BigTime

as a result of his participation in taking the company public. These facts are not disclosed in the

report but are disclosed on Excess Investment's Web site. Wilson decides, however, that the

timeliness of the information in the report warrants overlooking this issue so that the report can be

distributed.

Just before the report is issued. Holly mentions to Wilson that BigTime unknowingly disclosed to him

and a few other analysts who were wailing for a conference call to begin that the company is

planning to restructure both its sales staff and sales strategy and may sell one of its poorly

performing business units next year.

Three days after issuing his report on BigTime, which caused a substantial rise in the price of BigTime

shares, Holly sells all of the BigTirne shares out of both his performance fee-based accounts and

asset-based accounts and then proceeds to sell all of the BigTime shares out of his own account on

the following day. Holly obtained approval from Wilson before making the trades.

Just after selling his shares in BigTime, Holly receives a call from the CEO of BlueNote who wants to

see if Holly received the desk pen engraved with the BlueNote company logo that he sent last week

and also to offer two front row tickets plus limousine service to a sold-out concert for a popular band

that uses BlueNote's instruments. Holly confirms that the desk pen arrived and thanks the CEO for

the gift and tells him that before he accepts the concert tickets, he will have to check his calendar to

see if he will be able to attend. Holly declines the use of the limousine service should he decide to

attend the concert.

After speaking with the CEO of BlucNote, Holly constructs a letter that he plans to send by e-mail to

all of his clients and prospects with e-mail addresses and by regular mail to all of his clients and

prospects without e-mail addresses. The letter details changes to an equity valuation model that

Holly and several other analysts at Excess use to analyze potential investment recommendations.

Holly's letter explains that the new model, which will be put into use next month, will utilize Monte

Carlo simulations to create a distribution of stock values, a sharp contrast to the existing model

which uses static valuations combined with sensitivity analysis. Relevant details of the new model

are included in the letter, but similar details about the existing model are not included. The letter

also explains that management at Excess has decided to exclude alcohol and tobacco company

securities from the research coverage universe. Holly's letter concludes by stating that no other

significant changes that would affect the investment recommendation process have occurred or are

expected to occur in the near future.

Did Holly violate any CFA Institute Standards of Professional Conduct with respect to his report on

BlueNote or BigTime, as it relates to potential use of material nonpublic information?

Components (PCC). Although PCC has stable production output, the company is located in a

developing country with an uncertain economic environment. Since the monetary environment is

particularly worrisome. General has decided to approach the valuation of PCC from a free cash flow

model using real growth rates. In real rate analysis, General uses a modified build-up method for

calculating the required real return, specifically:

required real return = country real rate + industry adjustment +

company adjustment

Elias Sando, CFA, an analyst with General, estimates the following information for PCC:

Domestic inflation rate = 8.738%

Nominal growth rate = 12.000%

Real country return = 3.000%

Industry adjustmen = 3.000%

Company adjustment = 2.000%

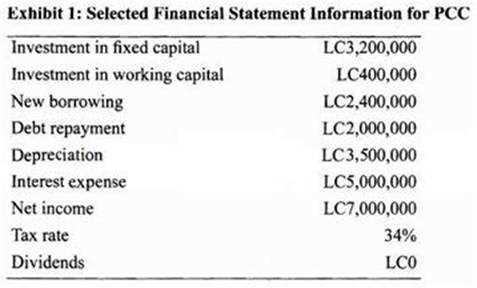

Additionally, Exhibit 1 reports information from PCC's financial statements for the year just ended

(stated in LC).

PCC generally maintains relatively constant proportions of equity and debt financing and is expected

to do so going forward.

Sando has gathered information on earnings before interest, taxes, depreciation, and amortization

(EBITDA) and is contemplating its direct use in another cash flow approach aimed at valuing PCC.

Consider the following two statements regarding EBITDA:

Statement 1: EBITDA is not a good proxy for free cash flow to the firm (FCFF) because it does not

incorporate the importance of the depreciation tax shield nor does it reflect the investment in

working capital or in fixed capital.

Statement 2: EBITDA is also a poor proxy for FCFE.

Under the assumption that PCC maintains relatively constant proportions of equity and debt

financing, the most appropriate valuation model is the:

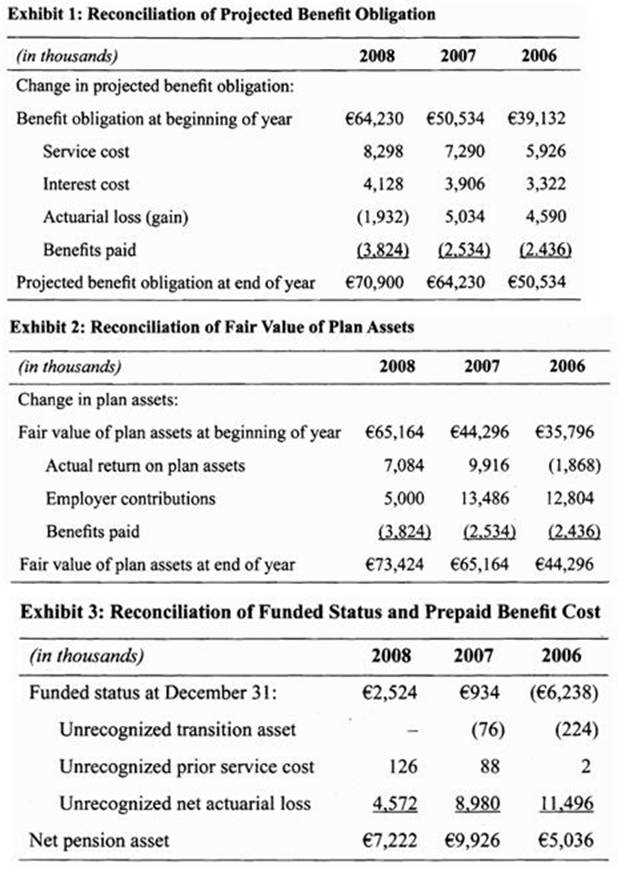

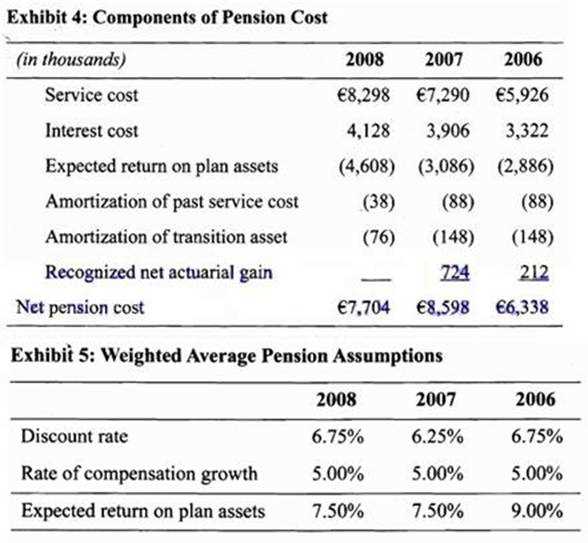

his attention is focused on the 2008 financial statements of Global Oilfield Supply, particularly the

footnote disclosures related to the company's employee benefit plans. Bostwick would like to adjust

the financial statements to reflect the actual economic status of the pension plans and analyze the

effect on the reported results of changes in assumptions the company used to estimate the projected

benefit obligation (PBO) and net pension cost. But first, Bostwick must familiarize himself with the

differences in the accounting for defined contribution and defined benefit pension plans.

Global Oilfield's financial statements are prepared in accordance with International Financial

Reporting Standards (IFRS). Excerpts from the company's annual report are shown in the following

exhibits.

What was the most likely cause of the actuarial gain reported in the reconciliation of the projected

benefit obligation for the year ended 2008?

of studies for her MBA, She took the Level 3 CFA® exam in June but has not yet received her score.

Garvey's work involves preparing research reports on small companies.

Garvey is at lunch with a group of co-workers. She listens to their conversation about various stocks

and takes note of a comment from Tony Topel, a veteran analyst. Topel is talking about Vallo

Engineering, a small stock he has tried repeatedly to convince the investment director to add to the

monitored list. While the investment director does not like Vallo, Topel has faith in the company and

has gradually accumulated 5,000 shares for his own account. Another analyst, Mary Kennedy, tells

the group about Koral Koatings, a paint and sealant manufacturer. Kennedy has spent most of the last

week at the office doing research on Koral. She has concluded that the stock is undervalued and

consensus earnings estimates are conservative. However, she has not filed a report for Samson, nor

does she intend to. She said she has purchased the stock for herself and advises her colleagues to do

the same. After she gets back to the office, Garvey purchases 25 shares of Vallo and 50 shares of

Koral for herself.

Samson pays its interns very little, and Garvey works as a waitress at a diner in the financial district

to supplement her income. The dinner crowd includes many analysts and brokers who work at

nearby businesses. While waiting tables that night, Garvey hears two employees of a major

brokerage house discussing Metrona, a nanotechnology company. The restaurant patrons say that

the broker's star analyst has issued a report with a buy rating on Metrona that morning. The diners

plans to buy the stock the next morning. After Garvey finishes her shift, restaurant manager Mandy

Jones, a longtime Samson client, asks to speak with her. Jones commends Garvey for her hard work

at the restaurant, praising her punctuality and positive attitude, and offers her two tickets to a

Yankees game as a bonus.

The next morning, Garvey buys 40 shares of Metrona for her own account at the market open. Soon

afterward, she receives a call from Harold Koons, one of Samson's largest money-management

clients. Koons says he got Garvey's name from Bertha Witt, who manages the Koons' account. Koons

wanted to reward the analyst who discovered Anvil Hammers, a machine-tool company whose stock

soared soon after it was added to his portfolio. Garvey prepared the original report on Anvil

Hammers. Koons offers Garvey two free round-trip tickets to the city of her choice. Garvey thanks

Koons, then asks her immediate supervisor, Karl May, about the gift from Koons but does not

mention the gift from Jones. May approves the Koons' gift.

After talking with May, Garvey starts a research project on Zenith Enterprises, a frozen-juice maker.

Garvey's gathers quarterly data on the company's sales and profits over the past two years. Garvey

uses a simple linear regression to estimate the relationship between GDP growth and Zenith's sales

growth. Next she uses a consensus GDP estimate from a well-known economic data reporting service

and her regression model to extrapolate growth rates for the next three years.

Later that afternoon, Garvey attends a company meeting on the ethics of money management. She

listens to a lecture in which John Bloomquist, a veteran portfolio manager, talks about his job

responsibilities. Garvey takes notes that include the following three statements made by Bloomquist:

Statement 1: I'm not a bond expert, and I've turned to a colleague for advice on how to manage the

fixed-income portion of client portfolios.

Statement 2: I strive not to favor either the remaindermen or the current-income beneficiaries,

instead I work to serve both of their interests.

Statement 3: All of my portfolios have target growth rates sufficient to keep ahead of inflation.

Garvey is not working at the diner that night, so she goes home to work on her biography for an

online placement service. In it she makes the following two statements:

Statement 1: I'm a CFA Level 3 candidate, and I expect to receive my charter this fall. The CFA

program is a grueling, 3-part, graduate-level course, and passage requires an expertise in a variety of

financial instruments as well as knowledge of the forces that drive our economy and financial

markets.

Statement 1: I expect to graduate with my MBA from Braxton College at the end of the fall semester.

As both an MBA and a CFA, I'll be in high demand. Hire me now while you still have the chance.

Did Garvey violate Standard 11(A) Material Nonpublic Information when she purchased Vallo and

Metrona?

largest market share in every city in which it competes. In its most successful large cities, Rogert has

as much as a 25% market share, although its share is sometimes greater in small cities. Rogert is

known for its excellent customer service and has a wide variety of grocery selections in almost every

part of its stores. Its profit margins on sales are slightly above industry averages, and its return on

assets and return on equity are above average.

Rogert has an equity beta of 0.78 and a debt-to-capital ratio of approximately 50%. Recent economic

difficulties, including higher commodity prices and higher unemployment, resulted in lower profit

margins for Rogert. Still, Rogert's decline in profit margin was less than for its competitors. Rogert did

not experience substantial losses of sales from customers switching to lower-priced competitors as

its market share remained substantially constant.

Zephine Markets is one of Rogert's smaller competitors. Zephine operates in roughly 15% of the

same cities as Roger. Zephine is publicly traded, and one of the members of Rogert's board of

directors has asked the staff to evaluate an acquisition of Zephine. The staff believes that Zephine is

slightly underpriced and that it could be acquired for a 20% premium over its current price. In

recommending against the acquisition, staff member Pierre Chiraq says:

"I agree that eliminating Zephine as a rival would probably enhance our profit margins. However, I

am skeptical about this acquisition. First, because our market share is almost never dominant, much

of the benefit of eliminating a smaller rival will be shared by our other rivals. They will free-ride on

our investment. Second, if our profit margins do increase, wc will eventually attract new rivals into

our markets. And finally, our cost of capital should increase substantially because the firm will be

diversifying horizontally instead of vertically, increasing the firm's risk."

Over the last several years, grocery industry growth has tended to follow the general economy. The

competitors in the industry, like Rogert, compete for market share in a stable industry. The industry's

cyclical behavior has shown stable performance in both the ups and downs of the business cycle.

In assessing Rogert's competitive position, Chiraq makes comments about the threat of new

entrants:

"My concern about new entrants into our business is low for several reasons. Economies of scale are

achievable at a low size of operations relative to that of our firm. Our brand identity is high in the

markets in which we compete. And, finally, access to distribution channels is difficult to achieve in

the grocery business. While there are many competitive forces that concern mc, new entrants is low

on my list."

Finally, the staff discusses industry changes that might have a negative effect on Rogert's industry

position. Three phenomena are mentioned that could have such an effect. They are:

1. Industry growth rates are low and declining;

2. Several suppliers are sponsoring national television advertisements for their products;

3. The government has approved a new method of extending the shelf life of fruits and vegetables.

Rogert's success can be attributed to: