Free AICPA CPA-Regulation Actual Exam Questions s

Dumps Box (DumpsBox) offers up-to-date practice exam questions for CPA-Regulation certification exam which are developed and validated by AICPA subject domain experts certified in AICPA CPA-Regulation s . These practice questions are update regularly as we keep an eye on any recent changes in CPA-Regulation syllabus, and when there is update our team quickly adjusts the questions. This commitment to providing the best quality exam prep material to certification aspirants is what makes DumpsBox.com the best certification exam prep website. On top of that, our strong, yet strictly moderated, community based feedback keeps the content clean and current. Each question has helpful community discussion that provides it extra perspective and introduces helpful resources for better exam preparation. This also saves students from other outdated practice questions or illicit exam dumps that can have adverse affects on career. Browse through our AICPA CPA-Regulation s exam questions and pass your exam on first try.

$20,000 for a new van. The new van had a fair market value of $10,000, and Leker also received

$3,000 in cash. What was Leker's tax basis in the acquired van?

had fire insurance coverage up to $500,000. Other pertinent information as of December 31, 1989

follows:

During January 1990, before the 1989 financial statements were issued, Pine received insurance

proceeds of $500,000. On what amount should Pine base the determination of its loss on involuntary

conversion?

following costs should be capitalized with respect to inventory if no exceptions are met?

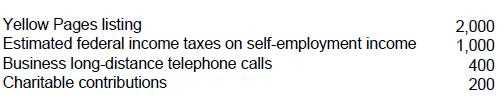

$20,000. Rich's cash disbursements were as follows:

What amount should Rich report as net self-employment income?

Gata's profits, losses, and capital. Gata is a distributor of auto parts. Wolf does not materially

participate in the partnership business. For the year ended December 31, 1989, Gata had an

operating loss of $100,000.

In addition, Gata earned interest of $20,000 on a temporary investment. Gata has kept the principal

temporarily invested while awaiting delivery of equipment that is presently on order. The principal

will be used to pay for this equipment. Wolf's passive loss for 1989 is:

accounts receivable were $25,000. During the year, Mosh collected $100,000 from customers. At the

end of the year, accounts receivable were $15,000. What was Mosh's gross taxable income for the

current year?

Guaranteed payment from services rendered to a partnership $50,000

Ordinary income from a S corporation $20,000

What amount of Freeman's income is subject to self-employment tax?

The child's cost basis in the stock at the date of sale was $16,000. Gibson sold the same stock to an

unrelated party for $18,000. What is Gibson's recognized gain from the sale?

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom’s daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom’s dependent. Determine the amount of income or loss, if any that should be included on page one of the Moores’ 1994 Form 1040. The Moores received $8,400 in gross receipts from their rental property during 1994. The expenses for the residential rental property were:

of college tuition for Clark's dependent child. One of the conditions that must be met for tax

exemption of accumulated interest on these bonds is that the:

In a tax year where the taxpayer pays qualified education expenses, interest income on the redemption of qualified U.S. Series EE Bonds may be excluded from gross income. The exclusion is subject to a modified gross income limitation and a limit of aggregate bond proceeds in excess of qualified higher education expenses. Which of the following is (are) true? I. The exclusion applies for education expenses incurred by the taxpayer, the taxpayer's spouse, or any person whom the taxpayer may claim as a dependent for the year. II. "Otherwise qualified higher education expenses" must be reduced by qualified scholarships not includible in gross income.